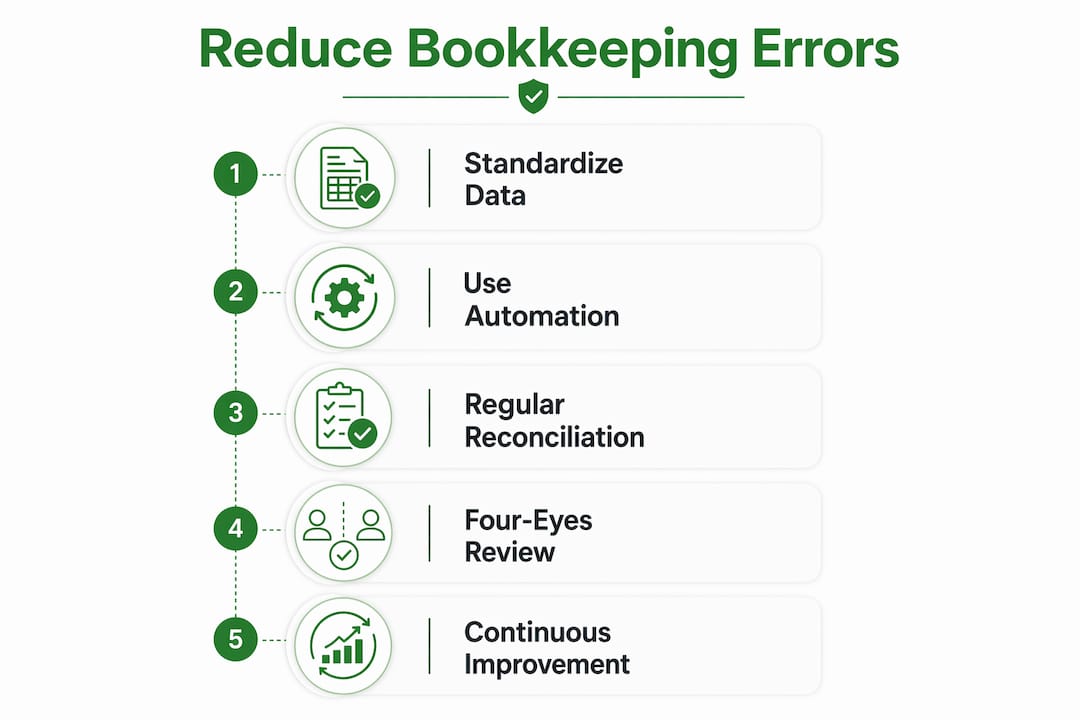

Proven Ways to Reduce Bookkeeping Errors Fast

Bookkeeping error reduction is defined as the systematic practice of applying standardized processes, automation, and structured review to prevent inaccurate financial records. Small business owners and freelancers who implement proven ways to reduce bookkeeping errors protect their cash flow, maintain tax compliance, and make decisions based on reliable data. The strategies covered here draw from professional bookkeeping standards, financial control frameworks, and real-world workflows. Each one is practical enough to apply immediately, regardless of your business size or accounting background.

Why standardized data formats are the foundation of accurate bookkeeping

Dirty data from inconsistent categorization is the primary cause of bookkeeping errors in cloud accounting environments. When transaction descriptions, vendor names, or account labels vary from month to month, errors multiply across every report that draws from that data. Standardizing your chart of accounts and categorization rules cuts dirty data at the source before it can create a cascading effect through your financial statements.

A standard chart of accounts gives every transaction a fixed home. Without it, the same office supply purchase might land under "office expenses" one month and "miscellaneous" the next, making reconciliation and tax prep far harder than they need to be. Predefined bank feed rules solve this by automatically assigning categories based on vendor name or transaction description patterns, removing the judgment call from daily entry.

Bookkeeping consistency reduces errors because it removes ambiguity. When every team member or automated rule follows the same naming convention and categorization logic, the system produces clean, comparable data month after month. This is why consistent data formats matter so much to bookkeepers working across multiple periods or clients.

Best practices for maintaining data consistency include:

- Use a single, locked chart of accounts and restrict changes to a designated administrator.

- Write categorization rules in plain language and document them in a shared reference file.

- Apply uniform vendor naming conventions so bank feed rules match reliably.

- Flag any uncategorized transactions in a dedicated review queue rather than forcing a quick guess.

- Review and update categorization rules quarterly to reflect new vendors or changed business activities.

Pro Tip: Audit your categorization rules every quarter. Business activities change, and rules built for last year's vendor mix will misfire on new transaction types.

How automation tools reduce manual entry errors

Automation removes judgment calls from daily entry, shifting the reviewer's focus to exceptions and trends rather than line-by-line data input. This shift reduces the volume of human decisions made per transaction, which directly lowers error risk. Automated bank feeds import transactions in real time, eliminating the manual transcription step where most entry mistakes occur.

AI-powered categorization takes automation further by learning from past decisions and suggesting categories based on transaction patterns. Anomaly detection flags duplicate entries, unexpected amounts, and transactions that fall outside normal ranges. These features do not replace human review, but they make that review faster and more targeted.

The table below shows common automation features and their direct impact on error reduction:

| Automation feature | How it reduces errors |

|---|---|

| Real-time bank feed import | Eliminates manual transcription of transaction data |

| Rule-based categorization | Applies consistent labels without human judgment per entry |

| Duplicate detection | Flags identical transactions before they post to the ledger |

| Anomaly flagging | Surfaces amounts or vendors that fall outside normal patterns |

| Automated invoice matching | Confirms payments against open invoices to prevent double payment |

Building rules for your top 20 transaction types during initial setup prevents error compounding from day one. This is the highest-risk period for automated bookkeeping because poorly configured rules replicate mistakes at scale. Spending time on setup pays back every month in cleaner data and faster closes.

Pro Tip: Combine automation with a weekly manual review of flagged exceptions. Automation handles volume; human review handles nuance.

What reconciliation frequency actually prevents

Monthly bank reconciliations reduce bookkeeping errors by 30% compared to less frequent schedules. That figure reflects how quickly discrepancies compound when left unaddressed. Reconciliation acts as an early warning system, surfacing fraud, duplicate charges, and misclassified transactions while the context is still fresh enough to resolve them quickly.

Professional bookkeeping standards recommend reconciling bank and credit card statements within 7 days for high-volume businesses. Weekly reconciliation keeps the gap between transaction date and review date short, which makes root cause identification far easier. Integrating bank feeds can cut reconciliation time significantly by pre-matching imported transactions against ledger entries.

A structured reconciliation workflow removes the guesswork. Follow this sequence to build one:

- Import all bank and credit card transactions for the period via your bank feed.

- Match each imported transaction against the corresponding ledger entry.

- Flag any unmatched transactions and assign them to a review queue.

- Investigate flagged items: confirm amounts, check for duplicates, and verify vendor identity.

- Reclassify any miscategorized transactions and document the correction reason.

- Run a variance report comparing the closing balance to the prior period.

- Sign off on the reconciliation with a dated record for audit purposes.

Common errors caught during reconciliation include duplicate vendor payments, bank fees posted to wrong accounts, timing differences from outstanding checks, and fraudulent charges on business credit cards. Each category has a distinct fix, and tracking which type appears most often reveals whether the problem is systemic or random.

Pro Tip: Set a recurring calendar reminder for reconciliation on the same day each week. Consistency in scheduling prevents the backlog that makes reconciliation feel like a crisis instead of a routine.

How a four-eyes review process catches what preparers miss

Independent double checks are critical because preparers develop blind spots to their own errors. A four-eyes review, where one person prepares the entries and a separate person reviews them, catches the mistakes that familiarity hides. This separation of duties is a core principle in professional bookkeeping quality control and applies equally to a two-person freelance operation and a larger accounting team.

A repeatable review process follows a defined sequence rather than a general scan. The reviewer checks transaction amounts against source documents, looks for round-dollar entries that may indicate estimates rather than actuals, and compares current-period totals against prior periods to identify unusual variance. Variance analysis is particularly effective because it surfaces both errors and genuine business changes that need explanation.

Key review activities and red flags to watch for:

- Round-dollar entries (e.g., exactly $500 or $1,000) that lack supporting documentation.

- Duplicate vendor names with slight spelling variations that bypass automated duplicate detection.

- Transactions posted to suspense or miscellaneous accounts without a follow-up note.

- Unusually large entries near period-end that could indicate timing manipulation.

- Missing receipts or invoices for transactions above your documentation threshold.

Structured workflows with documented exception handling and QA checklists are how professional firms maintain accuracy across teams. You can apply the same logic at a smaller scale by creating a one-page review checklist and requiring a dated sign-off before any period is closed.

Pro Tip: Wait at least 24 hours before self-reviewing your own entries. Distance from the work resets your attention and surfaces errors that felt invisible during preparation.

Troubleshooting common bookkeeping errors and improving over time

Root cause analysis with categorized exceptions significantly improves accuracy by revealing whether errors are systemic or isolated. Tracking exceptions by category, such as timing errors, misclassification, system errors, duplicate entries, and missing documentation, shows patterns that a simple error count cannot. When the same category appears repeatedly, the fix is a process change, not just a correction.

Analyzing error frequency over time separates random mistakes from structural problems. If misclassification errors spike every time you onboard a new vendor, the fix is a better onboarding checklist, not more careful typing. This distinction matters because process fixes scale; individual corrections do not.

Common bookkeeping mistakes and their corresponding fixes:

- Duplicate transactions: Set up automated duplicate detection rules and reconcile weekly to catch them before period close.

- Misclassified expenses: Review your chart of accounts quarterly and add new categories before new transaction types appear.

- Missing receipts: Implement a receipt capture habit at point of purchase using a mobile scanning app.

- Timing errors: Post transactions in the period they occurred, not when payment clears, and document accruals clearly.

- Uncategorized transactions: Create a zero-tolerance policy for suspense accounts and resolve them within 48 hours.

The highest error risk period in automated bookkeeping is initial setup. Errors introduced during configuration replicate automatically until someone catches and corrects the underlying rule. Scheduling a professional review 30 days after any new system setup catches these compounding errors before they distort a full quarter of data. You can find additional guidance on organizing business expenses to complement your error-reduction process.

Pro Tip: Engage a professional bookkeeper for a quarterly accuracy review, even if you handle day-to-day entries yourself. An outside perspective catches blind spots that internal review misses.

Key Takeaways

Reducing bookkeeping errors requires consistent data standards, well-configured automation, regular reconciliation, and a structured review process working together.

| Point | Details |

|---|---|

| Standardize data formats | A locked chart of accounts and uniform categorization rules prevent dirty data from compounding. |

| Configure automation carefully | Build rules for your top 20 transaction types at setup to prevent errors from replicating at scale. |

| Reconcile on a fixed schedule | Monthly reconciliation reduces errors by 30%; weekly is better for high-volume businesses. |

| Apply a four-eyes review | Independent review catches errors that preparers overlook due to familiarity with their own work. |

| Track errors by root cause | Categorizing exceptions reveals systemic process problems, not just individual mistakes. |

The case for keeping it simple before scaling it up

The most common mistake I see small business owners make is reaching for more automation before fixing their data hygiene. Automation amplifies whatever is already in your system. If your chart of accounts is inconsistent or your categorization rules are vague, automation will apply those inconsistencies faster and at greater volume than any human could.

My honest recommendation: spend one focused session standardizing your chart of accounts and writing your categorization rules in plain language before you connect a single bank feed. That foundation determines whether automation helps or hurts. I have watched businesses cut their monthly close time in half simply by fixing the rules layer, without adding any new software.

The four-eyes review is the other piece that gets skipped most often, especially by freelancers working alone. Even a self-review with a 24-hour gap between preparation and checking catches a meaningful number of errors. If you have a bookkeeper or accountant, formalize the handoff with a checklist and a sign-off requirement. The structure itself creates accountability that reduces errors before review even begins.

Automation is not the destination. It is the tool that frees you to focus on the exceptions that actually require judgment. Build the process first, then let technology handle the volume.

— Ian

Taxbatchpro automates the data capture that errors start from

The most error-prone step in bookkeeping is manual data entry from bank and credit card statements. Taxbatchpro eliminates that step entirely by converting scanned PDF statements into structured, tax-ready Excel spreadsheets in under 90 seconds. Transactions are automatically mapped to IRS Schedule C categories, removing the classification guesswork that produces dirty data.

Freelancers and small business owners can process a full year of statements in a single batch upload, arriving at reconciliation with clean, pre-categorized data rather than raw numbers that still need sorting. Accounting professionals can explore automated statement extraction built for their workflow, or use the free PDF conversion tool to see the accuracy difference firsthand. For tax-season readiness, the IRS-ready statement conversion service prepares clean financial data that holds up under audit.

FAQ

What are the most effective ways to reduce bookkeeping errors?

The most effective methods are standardizing your chart of accounts, automating bank feed imports with rule-based categorization, reconciling weekly or monthly, and applying a four-eyes review before closing any period. These four practices address the root causes of most bookkeeping errors.

How often should I reconcile my accounts to catch errors early?

Professional standards recommend reconciling within 7 days for high-volume businesses and at least monthly for all others. Monthly reconciliation alone reduces bookkeeping errors by 30% compared to less frequent schedules.

Why does consistent data formatting matter for bookkeeping accuracy?

Inconsistent formats create dirty data that multiplies errors across every report built from that data. A standardized chart of accounts and uniform categorization rules give automation and human reviewers a clean, reliable foundation to work from.

What is a four-eyes review in bookkeeping?

A four-eyes review is a quality control process where one person prepares entries and a separate person independently reviews them. This separation of duties catches errors that preparers miss due to familiarity with their own work.

When is automated bookkeeping most likely to produce errors?

The highest error risk period is initial system setup. Poorly configured categorization rules replicate mistakes automatically, so investing time in rule-building for your most frequent transaction types prevents compounding errors from the start.