Financial Record Retention: What Small Businesses Must Know

Financial record retention is defined as the systematic practice of keeping and managing business financial documents for legally required and operationally necessary time periods. For small business owners and finance professionals, understanding what is financial record retention means knowing exactly which documents to keep, for how long, and why the IRS cares deeply about both. The IRS audit statute of limitations runs a minimum of 3 years, but that window can extend significantly depending on your situation. A well-designed financial documents retention policy protects you from penalties, supports accurate bookkeeping, and gives you a defensible position if an audit arrives.

What is financial record retention and why does it matter?

Financial record retention is the structured process of preserving business financial documents according to legal mandates and business needs. The industry also refers to this practice as records management or document retention, and both terms appear in IRS guidance and legal frameworks. The importance of record retention goes beyond filing cabinets and cloud folders. Without a defined policy, small businesses risk destroying documents too early, retaining unnecessary data too long, or failing to produce records during an audit.

The IRS requires businesses to keep records that support every line on a tax return until the applicable statute of limitations expires. That standard period is 3 years from the filing date, but it extends to 6 years if income is underreported by more than 25%. In cases of suspected fraud or unfiled returns, there is no expiration at all. Those are not edge cases. They are real audit scenarios that small businesses face every year.

Record retention also supports daily financial record keeping. When transaction records are complete and organized, reconciliation is faster, tax prep is more accurate, and financial reporting carries more integrity. The cascading effect of poor retention shows up at the worst possible time: during an audit or a legal dispute.

What key financial records must small businesses retain and for how long?

Small businesses must retain several distinct categories of financial documents, each with its own recommended retention period. The IRS does not publish a single universal schedule, but its guidance combined with industry standards produces a clear framework.

Employment tax records must be kept for at least 4 years after the tax is due or paid, whichever is later. Many accounting professionals recommend extending that to 7 years for invoices, receipts, and accounts payable records to cover the full audit window. The logic is straightforward: a 7-year buffer covers both the standard 3-year period and the 6-year extension triggered by substantial income omission.

Some records carry no expiration date. Corporate formation documents, property deeds, annual financial statements, and board minutes must be retained permanently. These records establish legal existence and ownership history. Destroying them creates gaps that cannot be reconstructed.

| Document Category | Minimum Retention Period | Recommended Period |

|---|---|---|

| Federal and state tax returns | 3 years from filing date | 7 years |

| Bank and credit card statements | 3 years | 7 years |

| Invoices and receipts | 3 years | 7 years |

| Payroll and employment tax records | 4 years after tax due or paid | 7 years |

| Accounts payable and receivable | 3 years | 7 years |

| Corporate formation documents | Permanent | Permanent |

| Property deeds and titles | Permanent | Permanent |

| Annual financial statements | Permanent | Permanent |

| Board minutes and resolutions | Permanent | Permanent |

Pro Tip: When in doubt, default to 7 years for any document tied to income, deductions, or expenses. That single rule covers the IRS's 6-year extension window and removes the guesswork from most retention decisions.

How do federal tax laws and IRS guidelines impact financial record retention?

The IRS defines "adequate records" with specific precision. Every transaction must be supported by original documents showing the amount, date, place, and business purpose of the expense. Summaries and reconstructions do not satisfy this standard. The IRS expects source documents linked directly to the entries on your tax return.

The audit timeline structure creates three distinct retention scenarios:

- Standard 3-year period: Applies when income is fully reported and returns are filed on time. This covers the vast majority of small business audits.

- 6-year extended period: Triggered when gross income is understated by more than 25%. This is not limited to intentional errors. Honest omissions qualify too.

- Indefinite retention: Required when fraud is suspected or when no return was filed. There is no statute of limitations in these cases, which means records must be preserved without a defined end date.

- Employment tax records: The IRS requires a minimum of 4 years after the tax is due or paid. Payroll documentation falls into this category, including W-2s, 941 forms, and records of tax deposits.

Pro Tip: Never rely on your accounting software's summary reports as your primary audit evidence. The IRS expects original source documents, such as bank statements, receipts, and invoices, not just the numbers they produced.

The practical implication is that financial record keeping must capture transaction-level detail from the start. Reconstructing records after the fact is expensive, time-consuming, and often incomplete. Building the habit of retaining originals at the point of transaction is far more reliable than any recovery effort.

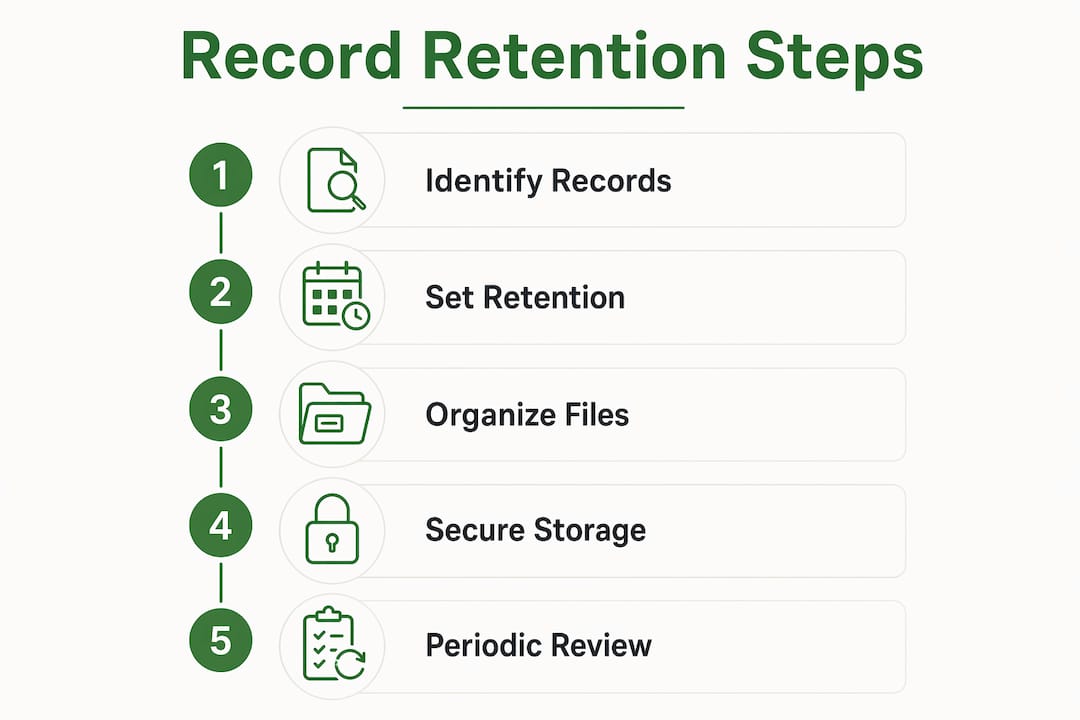

What are best practices for implementing a financial documents retention policy?

A financial documents retention policy is only as effective as its enforcement. A written policy that sits in a drawer provides no audit defense. The policy must be documented, distributed to staff, and applied consistently across all document types.

A written and enforced retention policy is one of the strongest protective measures available during an audit. It demonstrates a defensible, repeatable process to auditors and reduces the risk of penalties and interest charges. Auditors respond differently to businesses that can show a structured, documented approach versus those that produce records inconsistently.

Effective retention policies share several characteristics:

- Living schedules: Retention timelines should update when tax laws change, new regulations take effect, or the business's legal structure shifts. A static schedule created five years ago may no longer reflect current requirements.

- Data minimization: Balancing retention with data minimization reduces liability, storage costs, and complexity. Keeping every document indefinitely is not a safe strategy. It creates unnecessary exposure and inflates storage overhead.

- Litigation holds: When legal proceedings are anticipated or active, normal destruction schedules must be suspended immediately. This is called a litigation hold, and ignoring it can result in spoliation sanctions that are often more damaging than the underlying dispute.

- Staff training: Every employee who handles financial documents must understand the policy. Gaps in training create gaps in compliance.

- Secure disposal: Documents that have passed their retention period should be destroyed securely. Shredding physical records and permanently deleting digital files prevents unauthorized access to sensitive financial data.

Pro Tip: Schedule a formal policy review every January. Tax law changes, new IRS guidance, and shifts in your business structure can all affect retention requirements. An annual review keeps your policy current and defensible.

How can technology support financial record retention and audit readiness?

Digital document management removes the most common failure points in manual retention systems. Paper records get lost, misfiled, or damaged. Manual data entry introduces transcription errors that corrupt audit trails. Technology addresses both problems by capturing records at the source and storing them with searchable metadata.

Detailed source documents with transaction metadata are the foundation of a reliable audit trail. When digital accounting systems link original documents to summarized financial reports, auditors can trace every entry back to its source. That traceability is what the IRS means by "adequate records."

Secure backups and access controls are non-negotiable components of any digital retention system. A Written Information Security Plan (WISP) formalizes how financial data is stored, accessed, and protected. The IRS recommends that tax professionals maintain a WISP, and small businesses benefit from adopting the same standard.

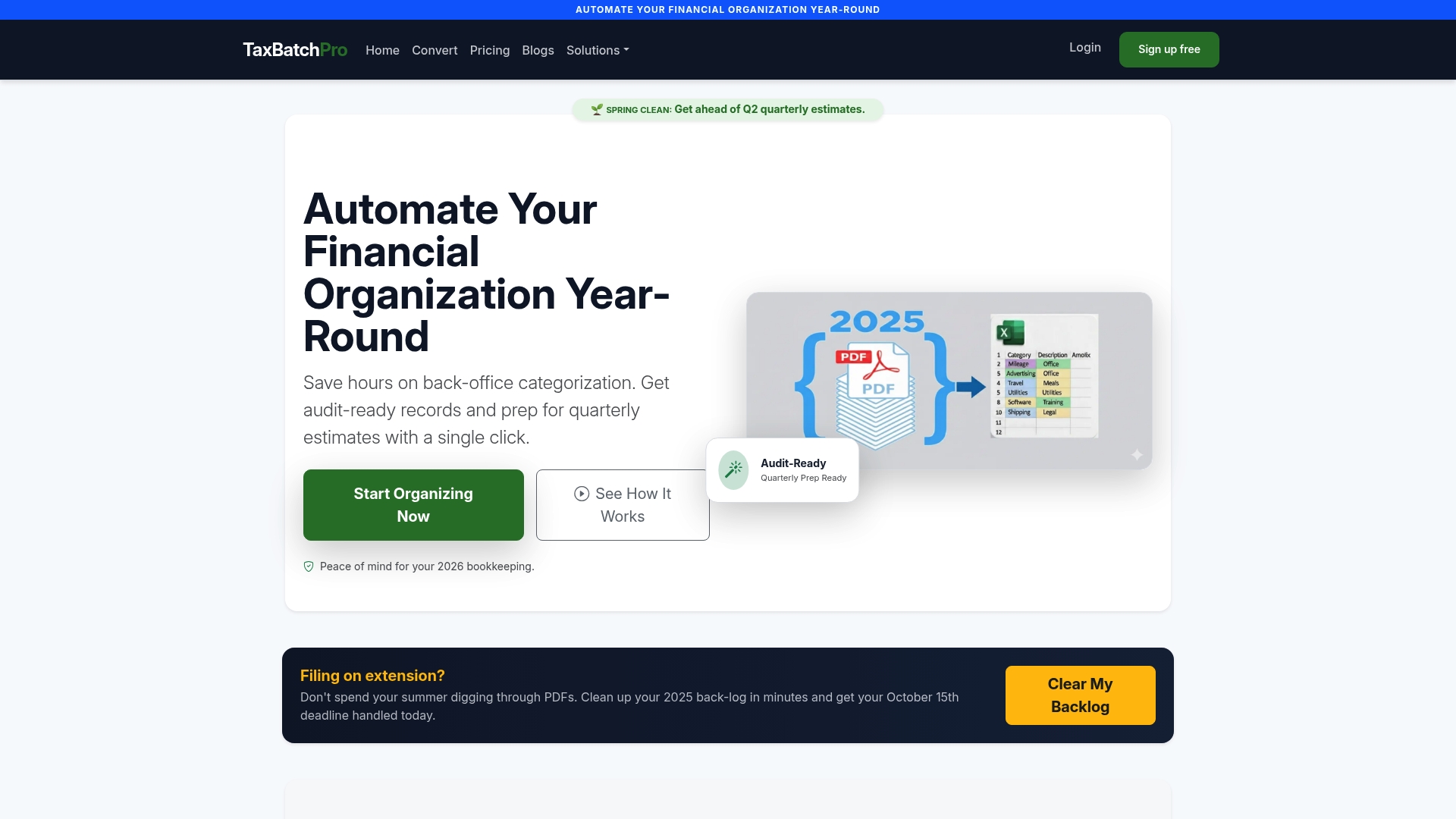

Taxbatchpro addresses a specific bottleneck in this process: converting scanned bank and credit card statement PDFs into structured, tax-ready Excel spreadsheets. The platform handles batch uploads, extracts transaction-level data, and maps entries to IRS Schedule C categories automatically. For small businesses managing a full year of statements, that process completes in under 90 seconds. The result is organized, IRS-ready documentation that supports both retention compliance and audit-ready bookkeeping.

What are common record retention pitfalls and how can they be avoided?

The most costly retention mistakes fall into two categories: destroying records too early and keeping everything indefinitely without a plan. Both create serious problems, though for different reasons.

Premature destruction is the more obvious risk. Destroying records during an active or anticipated legal proceeding triggers spoliation sanctions. Courts and the IRS treat missing records as evidence of wrongdoing, which shifts the burden of proof onto the business. The sanction is almost always worse than the original dispute.

Indefinite retention carries its own risks. Storing unnecessary documents increases storage costs, creates privacy exposure, and makes it harder to locate the records that actually matter. A business drowning in 20 years of unorganized files is not better protected than one with a clean, current retention schedule.

Common pitfalls to avoid:

- Skipping the litigation hold: When a dispute is anticipated, the destruction schedule stops. No exceptions.

- Relying on memory instead of policy: Verbal retention practices are not defensible. Every rule must be written down.

- Failing to audit the policy itself: A retention schedule that has not been reviewed in three or more years is likely out of date.

- Mixing personal and business records: Commingled records create reconciliation problems and weaken the audit trail for business expenses.

- Deleting digital files without verification: Confirm that records have passed their retention period before permanent deletion. A checklist prevents accidental destruction of documents still within their window.

Regular policy audits and staff training are the two most effective preventive measures. Both are low-cost investments compared to the expense of an audit defense built on incomplete records.

Key Takeaways

A well-enforced financial record retention policy, aligned with IRS guidelines and supported by digital tools, is the most reliable defense against audit penalties, legal sanctions, and bookkeeping errors.

| Point | Details |

|---|---|

| IRS retention baseline | Keep most tax-related records for at least 7 years to cover the standard and extended audit windows. |

| Permanent records exist | Corporate formation documents, property deeds, and board minutes must be retained indefinitely. |

| Written policy is required | A documented, enforced retention policy demonstrates compliance and reduces audit risk. |

| Litigation holds are mandatory | Suspend all record destruction immediately when legal proceedings are anticipated or active. |

| Technology closes the gap | Automated tools like Taxbatchpro convert statements into IRS-ready records and support data integrity. |

Why static retention policies are the real compliance risk

I have reviewed retention policies for dozens of small businesses over the years, and the most dangerous ones are not the businesses with no policy. The most dangerous ones are businesses with a policy they wrote in 2018 and never touched again. Tax law changes. Business structures change. The IRS updates its guidance. A static schedule does not adapt to any of that.

The businesses that handle audits well share one trait: they treat their retention policy as a living document, not a checkbox. They review it annually, update it when the law changes, and train their staff on it consistently. That discipline is not glamorous, but it is what separates a clean audit from a painful one.

Technology has made this easier than it has ever been. Platforms that automate statement extraction and categorization remove the manual transcription errors that corrupt audit trails. The data quality in financial reporting that used to require hours of reconciliation work now happens automatically. The businesses that adopt these tools are not just saving time. They are building a more defensible record from the first transaction.

My honest recommendation: stop treating record retention as a year-end task. Build it into your monthly workflow, automate what you can, and review your policy every january. The cost of doing it right is trivial compared to the cost of doing it wrong.

— Ian

How Taxbatchpro supports IRS-ready record retention

Staying audit-ready requires more than good intentions. It requires organized, structured financial records that trace every transaction back to its source document.

Taxbatchpro converts scanned bank and credit card statement PDFs into structured Excel spreadsheets, with transactions automatically mapped to IRS Schedule C categories. The platform processes a full year of statements in under 90 seconds, eliminating manual transcription and the errors that come with it. For accountants managing multiple clients, the statement extraction tools handle batch uploads and deliver IRS-ready output that supports both retention compliance and tax prep. Small businesses can also use the free PDF to Excel converter to get started without a commitment. Organized records from day one make every audit, filing, and reconciliation faster and cleaner.

FAQ

What is financial record retention?

Financial record retention is the practice of keeping business financial documents for legally required time periods to support tax compliance, audit readiness, and accurate bookkeeping. The IRS requires records to be kept until the applicable statute of limitations expires.

How long should small businesses keep financial records?

Most tax-related records should be kept for at least 7 years to cover both the standard 3-year IRS audit window and the 6-year extension that applies when income is underreported by more than 25%.

What records must be kept permanently?

Corporate formation documents, property deeds, annual financial statements, and board minutes must be retained permanently because they establish legal existence and ownership history.

What happens if you destroy records during an audit?

Destroying records during an active or anticipated legal proceeding triggers spoliation sanctions. Courts and the IRS treat missing records as evidence of wrongdoing, which typically results in outcomes worse than the original dispute.

What are retention requirements for employment tax records?

The IRS requires employment tax records to be kept for at least 4 years after the tax is due or paid. Most accounting professionals recommend extending that period to 7 years for added audit protection.