Accuracy in Tax Documentation: Your 2026 Compliance Guide

Accuracy in tax documentation is defined as the complete, verifiable alignment between reported income, claimed deductions, and supporting financial records. The role of accuracy in tax documentation goes far beyond bookkeeping hygiene. The IRS imposes a 20% accuracy-related penalty on underpayments caused by negligence or substantial understatement of income. That single penalty can erase months of profit for a freelancer or small business. Accurate records also determine how long the IRS can audit you. The standard audit window is three years, but omitting more than 25% of gross income extends that window to six years. Fraud or failure to file removes the time limit entirely.

What are the financial and legal consequences of inaccurate tax documentation?

Inaccurate tax records create a cascading effect that touches penalties, audit exposure, and lost deductions. The financial damage compounds quickly, and the legal exposure can follow a business for years.

The IRS treats poor recordkeeping as negligence. Negligence is not just carelessness. It is a legal finding that triggers the 20% underpayment penalty on the portion of tax owed that was understated. For a business with a $10,000 underpayment, that is a $2,000 penalty before interest accrues.

The consequences of inaccurate records fall into three categories:

- Disallowed deductions. If you cannot substantiate an expense with a receipt, invoice, or bank record, the IRS can remove it. Removing deductions increases taxable income and the resulting tax bill.

- Extended audit windows. When income omissions exceed 25% of gross income, the statute of limitations doubles from three to six years. Fraud eliminates the deadline entirely.

- Automated scrutiny. The IRS Automated Underreporter program matches reported income against third-party documents like 1099s and bank statements. Any mismatch flags your return for review.

The legal implication of negligence is significant. The IRS defines failure to keep adequate records as a form of disregard for tax rules. That classification opens the door to penalties beyond the standard underpayment rate.

Pro Tip: Reconcile your bank statements to your income records monthly. Catching a mismatch in february is far less costly than discovering it during an audit in october.

Understanding why bookkeeping errors trigger audits gives you a clearer picture of how the IRS selects returns for review and what you can do before filing to reduce that risk.

How does accuracy in tax documentation contribute to smoother audits?

Tax authorities operate from a position that every claimed deduction must be proven. Documentation is the primary defense against disallowed expenses and escalating penalties. Taxpayers with organized, reconciled records resolve audits faster and with narrower scope.

The IRS audit process focuses on three reconciliation points: reported income versus bank deposits, claimed deductions versus receipts and invoices, and general ledger entries versus financial statements. Discrepancies between bank deposits and reported income are one of the fastest audit triggers the IRS uses. Consistent reconciliation across all three points closes that gap before it becomes a problem.

The quality of your records directly shapes the audit outcome. The table below shows how documentation quality affects audit scope and penalty risk.

| Record quality | Audit scope | Penalty risk |

|---|---|---|

| Fully reconciled, organized records | Limited, targeted review | Low |

| Partially organized, some gaps | Expanded review of affected years | Moderate |

| Disorganized, missing documents | Broad, multi-year audit | High |

| No records or reconstructed after the fact | Full examination, potential fraud referral | Very high |

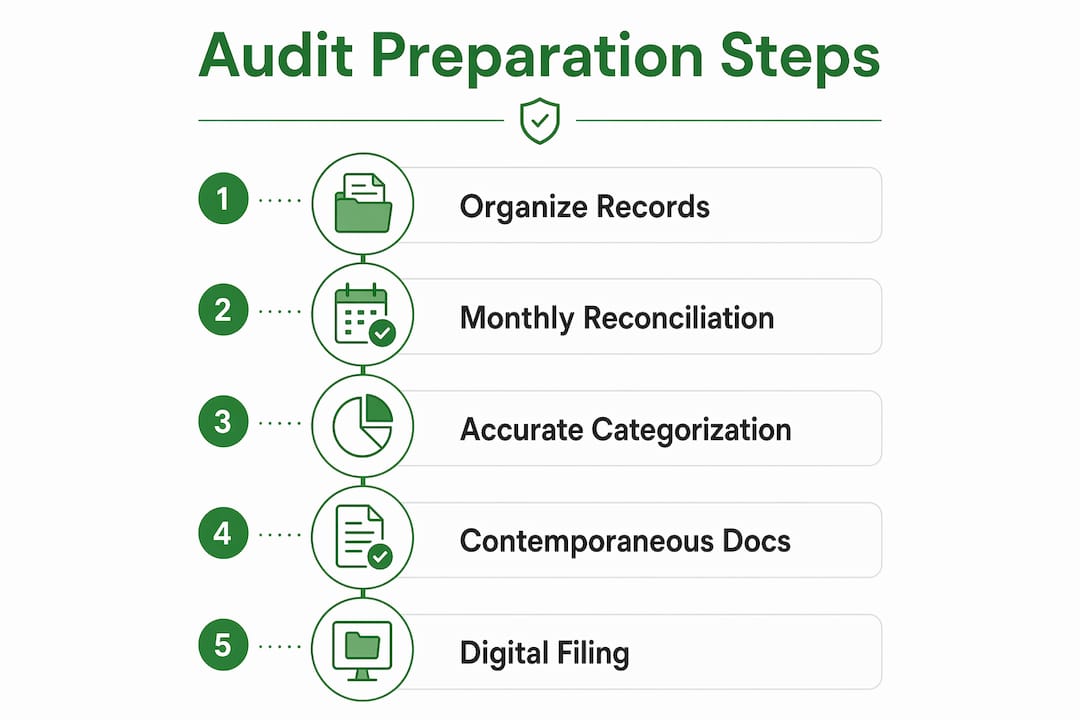

Contemporaneous documentation is the most effective audit defense available. Records created at the time of a transaction carry far more weight than records reconstructed weeks or months later. The IRS routinely rejects after-the-fact documentation as insufficient to substantiate expenses.

Accurate expense categorization also matters. When deductions are mapped to the correct IRS Schedule C categories, auditors can verify them quickly. Miscategorized expenses invite deeper scrutiny, even when the underlying amounts are correct.

Pro Tip: Keep a digital folder for each month with bank statements, receipts, and a reconciliation summary. If an audit arrives, you hand over the folder rather than spending weeks reconstructing records.

What are the best practices for maintaining accuracy in tax records?

Precision in tax records does not happen by accident. It requires consistent habits, the right systems, and early error detection. The good news is that modern tools have made this far more achievable than it was even five years ago.

The core practices that protect data integrity are:

- Monthly reconciliation. Match every bank and credit card transaction to your general ledger at the end of each month. Do not wait until tax season.

- Structured digital storage. Organize records by year, month, and category. A consistent folder structure means you can locate any document within seconds.

- Cross-source verification. Compare income reported on 1099s and invoices against actual bank deposits. Any gap needs an explanation before filing.

- Automated data extraction. Structured, API-driven recordkeeping systems have reduced manual validation exception resolution time by 70% in documented case studies. That reduction means fewer errors reaching your tax return.

- Early error correction. Errors caught before filing cost nothing beyond the time to fix them. Errors caught during an audit cost penalties, interest, and professional fees.

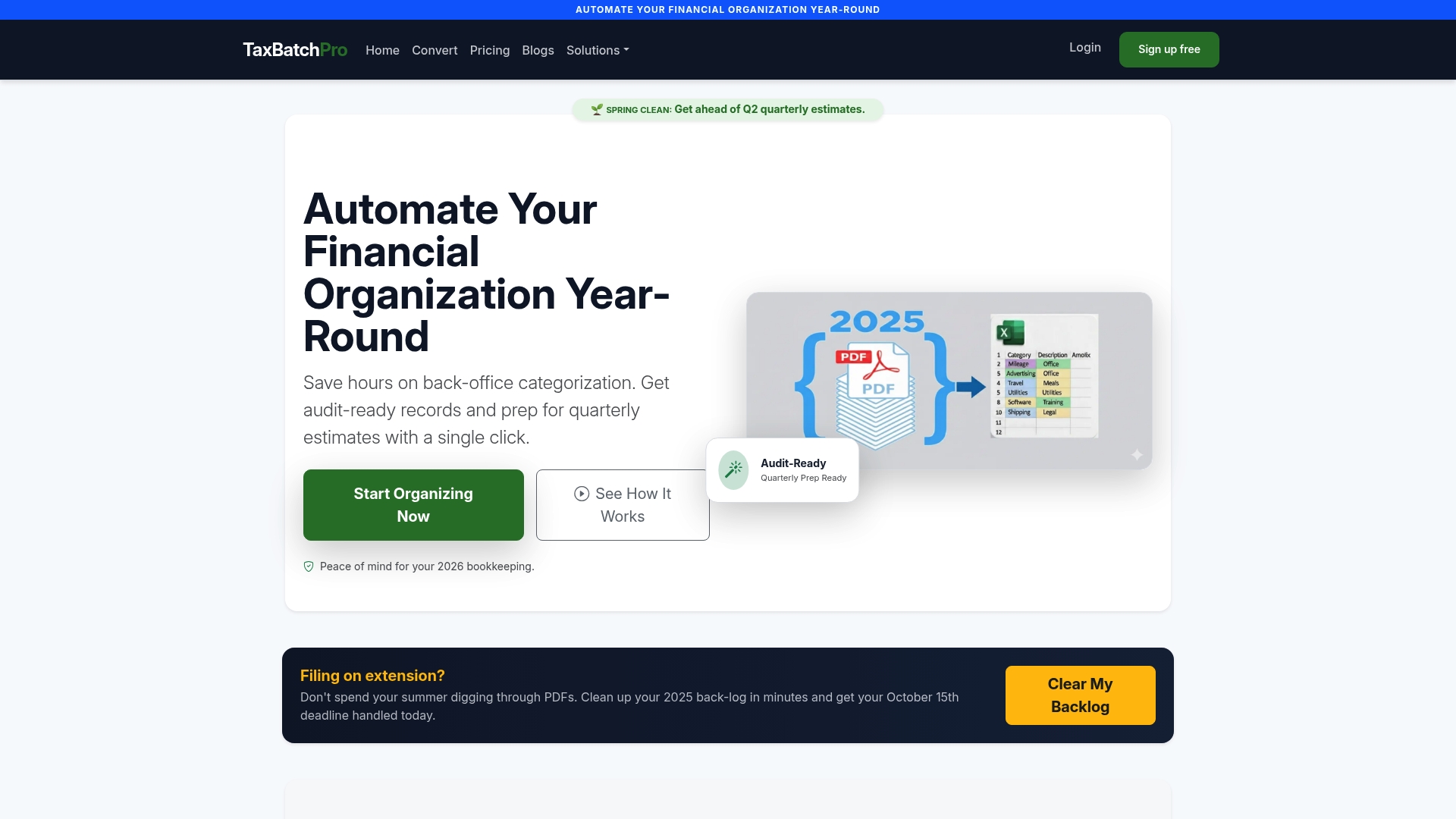

AI-powered tools now handle the most error-prone step in bookkeeping: manual transcription. Platforms like Taxbatchpro convert scanned bank and credit card statement PDFs into structured, IRS-ready Excel spreadsheets, automatically mapping transactions to Schedule C categories. That removes the manual entry step where most data integrity failures occur.

Reducing bookkeeping errors at the source is more effective than reviewing for errors after the fact. Build verification into your monthly workflow rather than treating it as a year-end task.

Pro Tip: Set a recurring calendar reminder on the first business day of each month to reconcile the prior month's statements. Thirty minutes monthly prevents thirty hours of reconstruction at tax time.

For a deeper look at how data quality supports real-time financial reporting, the principles of validation and error prevention apply directly to tax documentation as well.

How do evolving tax regulations affect the importance of accurate records?

Tax compliance requirements are tightening globally, and the United States is not isolated from that trend. Accurate recordkeeping has moved from a best practice to a legal obligation in multiple jurisdictions.

The UAE Corporate Tax regime, introduced as a reference point for integrated compliance, illustrates a broader shift. Accounting accuracy directly impacts taxable income calculation under that framework, and errors expose businesses to penalties regardless of intent. The United States follows a similar logic through IRS penalty structures that treat negligence and accuracy failures as equivalent in their financial consequences.

"The division between financial reporting and tax accounting is disappearing. Maintaining accurate records is now fundamental for tax compliance, not just good financial management. Businesses that treat their accounting records as a tax compliance tool, rather than a separate administrative function, are better positioned to meet audit demands and avoid penalties."

This convergence means that financial statements and tax returns must tell the same story. Mismatches between the two are audit triggers. Timing errors, where income or expenses are recorded in the wrong period, create discrepancies that automated IRS systems detect quickly.

The practical response is an integrated approach: use the same records for financial reporting and tax preparation. Audit-ready financial statements with full supporting documentation satisfy both obligations simultaneously. Regular tax-focused reviews, conducted quarterly rather than annually, catch timing and classification errors before they compound.

Pro Tip: Schedule a quarterly tax review with your accountant or bookkeeper. Reviewing four smaller periods is faster and less expensive than untangling a full year of misclassified transactions in april.

Tax return accuracy best practices for CPAs in 2026 covers how professionals are adapting their workflows to meet these rising compliance standards.

Key takeaways

Accuracy in tax documentation is the single most effective defense against IRS penalties, audit escalation, and lost deductions. Build it into your monthly workflow, not your year-end scramble.

| Point | Details |

|---|---|

| IRS accuracy penalty | A 20% penalty applies to underpayments caused by negligence or substantial income understatement. |

| Audit window extension | Omitting more than 25% of gross income extends the IRS audit window from three to six years. |

| Contemporaneous records | Records created at the time of a transaction are the strongest audit defense available. |

| Monthly reconciliation | Reconciling bank statements to your ledger monthly prevents errors from compounding into penalties. |

| Automation reduces errors | Structured, automated recordkeeping systems cut manual validation errors and protect data integrity. |

Why accuracy is the one thing I never compromise on

Tax professionals talk a lot about efficiency. I have spent years watching that conversation miss the point. Efficiency without accuracy is just a faster way to create problems.

The most common audit trigger I see is not aggressive deductions. It is simple reconciliation failures. A freelancer deposits $85,000 in a year but reports $72,000 because a few client payments were miscategorized as reimbursements. The IRS Automated Underreporter program flags it within weeks of filing. The audit that follows is not about the $13,000 gap. It is about every other number on that return.

Accuracy is a competitive advantage for tax professionals, not just a compliance checkbox. When your records are clean, you spend your time on planning and strategy. When they are not, you spend it on damage control.

The habit that matters most is contemporaneous documentation. Record the purpose of every expense at the time you incur it. A note in your phone, a tagged receipt in a folder, a memo line in your accounting software. After-the-fact reconstruction is always weaker, always slower, and often insufficient to satisfy an auditor.

Technology has made this easier than it has ever been. There is no longer a good reason to rely on manual transcription for bank statement data. The tools exist to eliminate that bottleneck entirely.

— Ian

Taxbatchpro: built for accurate, IRS-ready tax documentation

Accurate tax records start with clean, structured data. Taxbatchpro converts scanned bank and credit card statement PDFs into IRS-ready Excel spreadsheets in under 90 seconds, automatically mapping every transaction to the correct IRS Schedule C category. There is no manual transcription, no reformatting, and no guessing about which category applies.

For freelancers and small business owners, Taxbatchpro processes a full year of statements in a single batch upload. For accountants managing multiple clients, the platform handles volume without sacrificing accuracy. Review the available pricing plans to find the option that fits your workflow. Your records will be organized, reconciled, and ready before the IRS ever asks.

FAQ

What is the IRS penalty for inaccurate tax documentation?

The IRS imposes a 20% accuracy-related penalty on the portion of tax underpayment caused by negligence or substantial understatement of income. This penalty applies in addition to any interest owed on the unpaid amount.

How long can the IRS audit a return with inaccurate records?

The standard IRS audit window is three years. If a taxpayer omits more than 25% of gross income, that window extends to six years, and there is no time limit if fraud or failure to file is involved.

What counts as contemporaneous documentation for tax purposes?

Contemporaneous documentation means records created at the time of a transaction, such as receipts, invoices, and bank statements with memo notes. Records reconstructed after the fact are generally insufficient to substantiate deductions during an audit.

How does reconciliation reduce audit risk?

Regular reconciliation aligns bank deposits, general ledger entries, and reported income so that no discrepancies exist for automated IRS systems to flag. Consistent reconciliation is one of the most direct ways to reduce the likelihood of audit selection.

Can automation improve the accuracy of tax records?

Structured, automated recordkeeping systems have reduced manual validation exception resolution time by 70% in documented case studies. Automation removes the manual transcription step where most data integrity errors originate.