Quarterly Estimated Tax Recordkeeping Guide for Freelancers

Quarterly estimated tax recordkeeping is the practice of systematically tracking income, expenses, and IRS payments each quarter to meet federal compliance requirements and avoid underpayment penalties. The IRS requires estimated tax payments from any taxpayer who expects to owe at least $1,000 in taxes after credits and withholding. For 2026, the payment deadlines fall on april 15, june 15, september 15, and january 15 of the following year. Accurate records support every step of this process: calculating what you owe, verifying what you paid, and defending your position if the IRS ever questions a return.

What records are essential for quarterly estimated tax tracking?

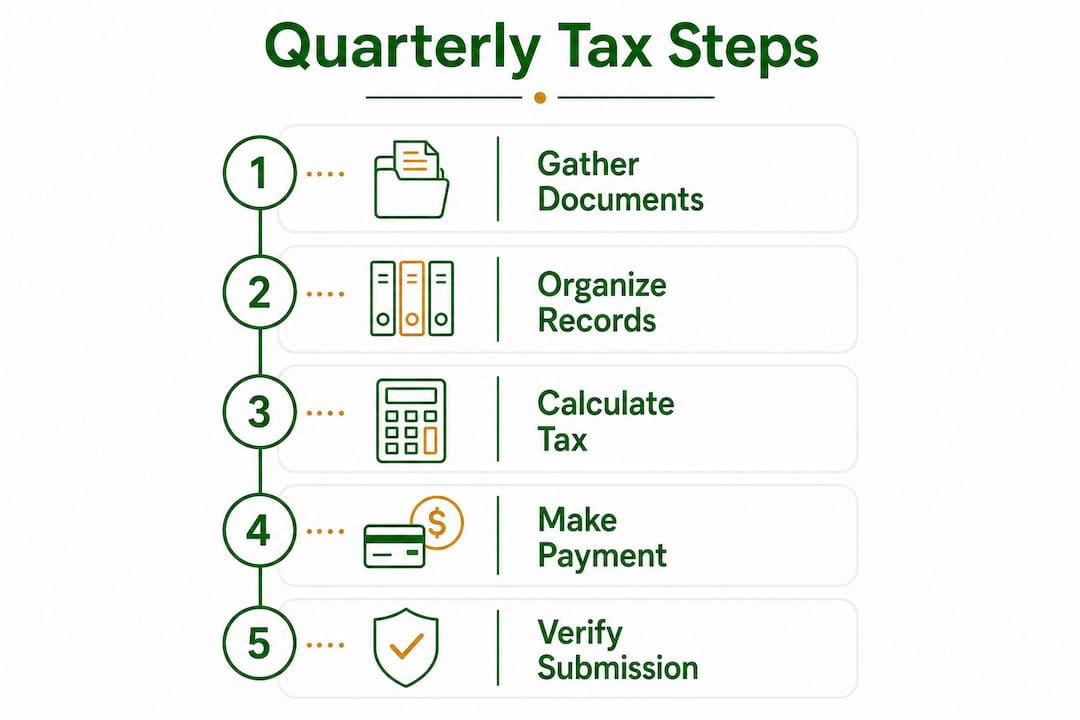

Effective quarterly estimated tax recordkeeping starts with five categories of documentation. Each category serves a specific function in the compliance chain, and missing any one of them creates gaps that compound over time.

- Income proof: Invoices, 1099-NEC forms, payment processor reports, and direct deposit records. These establish your gross receipts for each quarter.

- Expense documentation: Receipts, bank statements, and credit card records tied to deductible business costs. Proper expense organization directly reduces your taxable income and, by extension, your quarterly payment obligation.

- Calculation worksheets: IRS Form 1040-ES worksheets or equivalent digital records showing how you arrived at each payment amount. These are your audit trail for the math.

- Payment confirmations: Confirmation numbers from IRS Direct Pay or EFTPS, bank transaction records, and timestamps. Without these, you cannot prove a payment was made on time.

- Assumption notes: A brief internal memo per quarter explaining any estimates, income projections, or adjustments you made. This is the record most freelancers skip, and it is the one that matters most when income shifts unexpectedly.

Organizing digital folders by quarter, such as "2026 Q1 Tax Records," and updating them progressively throughout the quarter prevents the end-of-deadline scramble. The folder closes when the payment is confirmed, not when the deadline passes.

Pro Tip: Set a recurring calendar event two weeks before each deadline to review and close your quarterly folder. Waiting until the due date leaves no room to catch errors.

How to calculate your quarterly estimated tax payments accurately

Two calculation methods govern most estimated tax situations. Choosing the right one depends on how predictable your income is.

- Prior-year safe harbor method: Base your payments on last year's total tax liability. Pay at least 100% of that amount across four installments. If your adjusted gross income exceeded $150,000 last year, the threshold rises to 110%.

- Current-year 90% method: Estimate your actual current-year tax liability and pay at least 90% of it. This method requires more frequent income monitoring but produces more accurate payments when income is rising.

- Annualized income installment method: Calculate each payment based on actual income earned through that specific quarter. This method requires IRS Form 2210 Schedule AI and is the best option for freelancers with seasonal or highly variable revenue.

The safe harbor rules exist to protect you from penalties, not to optimize your payments. Underpayment penalties accrue from the due date at approximately 8% annually, calculated on the shortfall. That rate makes underpayment genuinely expensive, not just inconvenient.

A common mistake is relying solely on prior-year data without adjusting for a significant income change. If your revenue grew substantially this year, the prior-year safe harbor may still protect you from penalties, but you will face a large balance due in april. Adjusting based on current-year income reduces both penalties and cash flow stress at filing time.

Your quarterly payment must cover both income tax and self-employment tax. Self-employment tax runs at 15.3% on net self-employment income up to the Social Security wage base, then 2.9% above it. Many freelancers underestimate their liability by forgetting this component entirely.

Pro Tip: Run a quick income-versus-prior-year comparison at the start of each quarter. If your year-to-date revenue is tracking more than 20% above last year, switch to the current-year 90% method for that quarter.

Best practices for organizing and verifying quarterly tax payments

Payment execution and record maintenance are two separate tasks. Both require discipline.

Payment options and documentation:

- IRS Direct Pay: free, immediate, and generates a confirmation number you should save the same day.

- EFTPS (Electronic Federal Tax Payment System): best for businesses making recurring payments; allows scheduling in advance.

- Credit or debit card: processed through IRS-approved third-party processors; a convenience fee applies.

- Mail check: the riskiest option because delivery confirmation is difficult. If you use it, send via certified mail and retain the receipt.

Verification via your IRS Individual Online Account is the step most freelancers skip. The IRS account shows payment history for up to five years and confirms whether a payment posted correctly. A payment that left your bank account is not necessarily a payment the IRS has credited to the correct tax year. Checking this within a week of each deadline catches posting errors before they become reconciliation problems.

Reconcile three sources every quarter: your internal ledger or spreadsheet, your bank records, and your IRS account. Discrepancies between any two of these signal a problem that needs resolution before the next quarter opens.

Pro Tip: Keep a dedicated tax savings account and transfer a fixed percentage of every payment you receive into it immediately. Separating tax funds from operating cash prevents accidental spending and makes quarterly payments predictable.

The table below summarizes the 2026 quarterly deadlines and the income periods each payment covers.

| Quarter | Income period | Payment deadline |

|---|---|---|

| Q1 | January–March | April 15, 2026 |

| Q2 | April–May | June 15, 2026 |

| Q3 | June–August | September 15, 2026 |

| Q4 | September–December | January 15, 2027 |

Note that quarterly periods are uneven. Q2 covers only two months. This catches many freelancers off guard when their Q2 payment feels disproportionately large relative to the income period.

How to adjust your recordkeeping when income or expenses change mid-year

Income volatility is the norm for freelancers, not the exception. Your recordkeeping system must accommodate changes without breaking down.

- Review income trends at the start of each quarter. Compare your year-to-date revenue against the same period last year and against your original annual projection. A 15% or greater variance is a signal to recalculate.

- Update your assumption notes immediately. When you revise an estimate, document why. Note the date, the trigger (a lost client, a new contract, a slow month), and the revised projection. This creates a defensible paper trail.

- Switch calculation methods if warranted. The annualized income installment method protects you from penalties during volatile periods. It requires more documentation, but the penalty savings justify the effort for freelancers with seasonal revenue patterns.

- Account for new deductions mid-year. If you purchase equipment, start a home office, or add a retirement contribution, update your expense records and recalculate your taxable income for the remaining quarters. A self-employed tax prep checklist helps you catch deductions you might otherwise miss.

- Check state requirements separately. State estimated tax rules vary significantly. Some states require quarterly payments at lower income thresholds than the federal $1,000 rule. Others have different deadlines. Treat state compliance as a parallel recordkeeping obligation, not an afterthought.

- Understand that extensions do not move payment deadlines. A filing extension gives you more time to submit your return, not more time to pay. Estimated payments remain due on their original dates regardless of any extension you file.

The most common mid-year mistake is waiting until Q4 to reconcile a full year of income changes. By that point, three quarters of potential penalties have already accrued. Quarterly reconciliation, not annual, is the standard that protects you.

Key takeaways

Accurate quarterly estimated tax recordkeeping requires five categories of documentation, consistent reconciliation across three sources, and a calculation method matched to your income pattern.

| Point | Details |

|---|---|

| Know the $1,000 threshold | Estimated payments are required when you expect to owe at least $1,000 after credits and withholding. |

| Match your calculation method to income | Use the annualized installment method for volatile income; use safe harbor for stable, predictable revenue. |

| Verify payments with the IRS | Check your IRS Individual Online Account after each payment to confirm correct posting. |

| Close each quarterly folder on time | Save confirmation numbers, bank records, and assumption notes before the next quarter opens. |

| Track state rules separately | State thresholds and deadlines differ from federal rules and require their own compliance records. |

Why I treat quarterly taxes as a forecasting discipline, not a filing task

Most freelancers I have worked with treat estimated taxes as a deadline problem. They scramble every three months, make a rough payment, and move on. That approach works until it doesn't, and when it fails, it fails expensively.

The mental shift that changes everything is treating estimated taxes as continuous forecasting. You are not filing a return four times a year. You are updating a rolling projection of your annual liability based on real data. That framing changes how you maintain records, because forecasters document their assumptions. They note when projections change and why.

The verification step via the IRS Individual Online Account is the one I see skipped most often, even by experienced freelancers. A payment that cleared your bank is not automatically a payment the IRS credited correctly. I have seen payments applied to the wrong tax year because of a data entry error at the payment processor. Catching that in week one costs you nothing. Catching it in april costs you time, stress, and potentially a penalty dispute.

The other habit worth building is the quarterly reset. The moment a payment is confirmed, close that quarter's folder. Archive it. Start the next one fresh. This prevents the cascading effect where one quarter's unresolved discrepancy contaminates the next quarter's calculation. Consistent financial record retention is not bureaucratic overhead. It is the foundation of accurate tax math.

— Ian

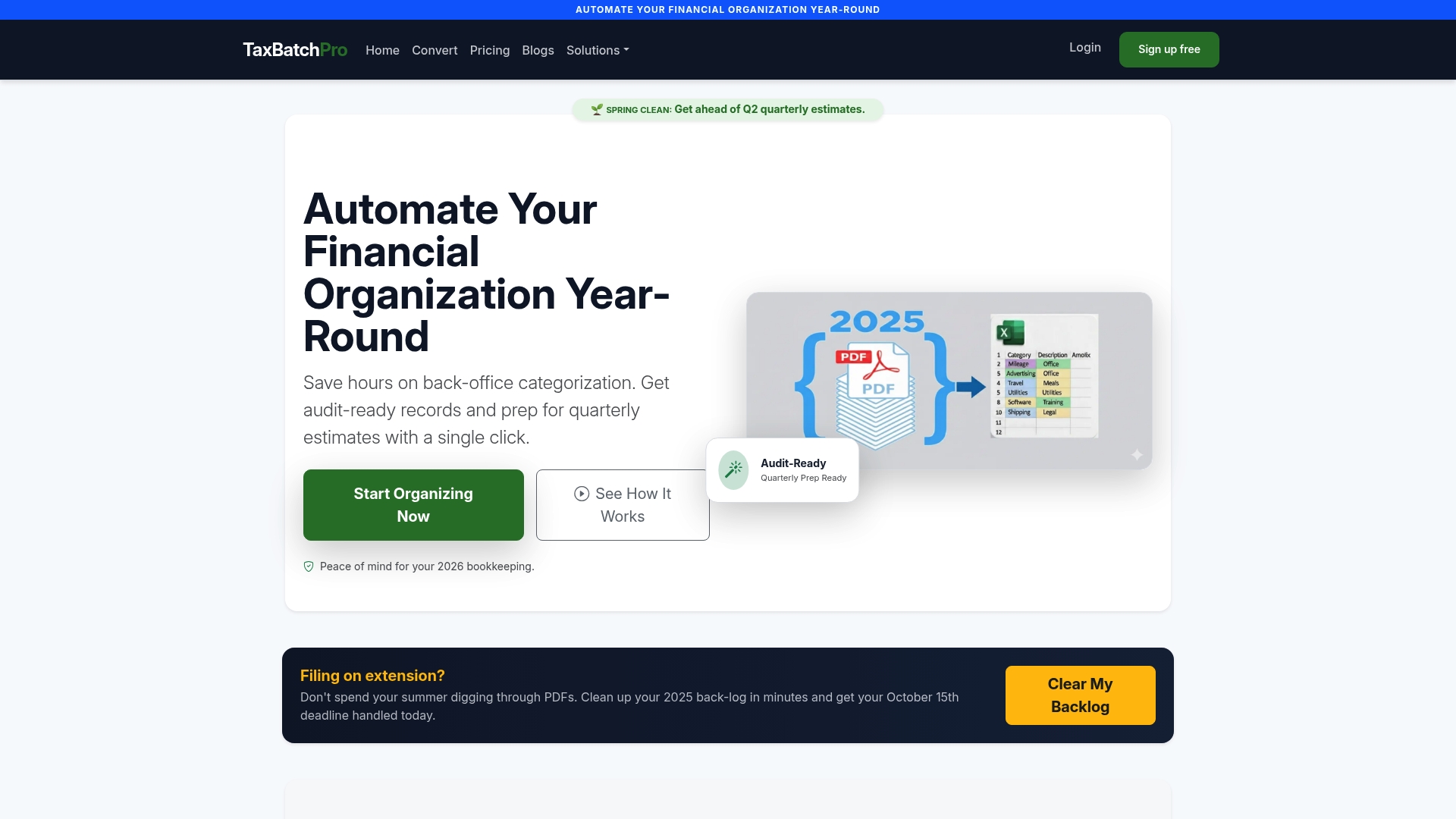

Taxbatchpro makes quarterly tax recordkeeping faster and more accurate

Freelancers and small business owners spend significant time manually pulling transaction data from bank and credit card statements to support their quarterly calculations. Taxbatchpro eliminates that bottleneck.

Taxbatchpro converts scanned bank and credit card statement PDFs into structured, IRS-ready Excel files in under 90 seconds. Transactions are automatically mapped to IRS Schedule C categories, so your expense documentation is organized and calculation-ready before the quarterly deadline arrives. Batch uploads handle a full year of statements at once, which means your reconciliation process starts with clean, structured data rather than raw PDFs. For freelancers who want to move faster without sacrificing accuracy, Taxbatchpro's conversion tool is a direct solution to the most time-consuming part of quarterly tax prep.

FAQ

What triggers the requirement to pay quarterly estimated taxes?

You must make quarterly estimated tax payments if you expect to owe at least $1,000 in federal taxes after withholding and credits. Self-employed individuals and freelancers typically meet this threshold because no employer withholds taxes on their behalf.

What is the safe harbor rule for estimated taxes?

The safe harbor rule protects you from underpayment penalties if you pay at least 90% of your current-year tax liability or 100% of last year's liability. The threshold rises to 110% of last year's liability if your prior-year adjusted gross income exceeded $150,000.

What happens if I miss a quarterly estimated tax deadline?

Missing a quarterly payment triggers a penalty calculated from the due date to the date you pay, or to the following april 15, whichever comes first. The penalty accrues at approximately 8% annually on the underpaid amount.

How do I verify that the IRS received my estimated tax payment?

Log in to your IRS Individual Online Account at irs.gov to confirm payment posting. The account displays payment history for up to five years and shows whether each payment was applied to the correct tax year.

Does a tax filing extension also extend my quarterly payment deadlines?

No. A filing extension gives you more time to submit your annual return, but estimated payment deadlines remain fixed. You must pay by each quarterly due date regardless of any extension you have filed.